Technical Indicators

MACD Zero Lag

The MACD Zero Lag (also known as zero lag MACD) is a variant of the classic MACD indicator. This variant was developed by Patrick Mulloy and presented in his book Stocks & Commodities in 1994.

Compared to the classic MACD, the MACD Zero Lag provides earlier signals. However, as it reacts more quickly to price changes, the risk of getting false signals is higher.

Calculation Method

MACD-ZL = (2 * EMA(closing price, St) - EMA(EMA(closing price, St), St))

- (2 * EMA(closing price, Lt) - EMA(EMA(closing price, Lt), Lt))

Trigger = (2 * EMA(MACD-ZL, Tr) - EMA(EMA(MACD-ZL, Tr), Tr))

where:

- St: short period

- Lt: long period

- Tr: trigger period

- EMA(closing price, St): Exponential Moving Average of closing prices with period St

- EMA(closing price, Lt): Exponential Moving Average of closing prices with period Lt

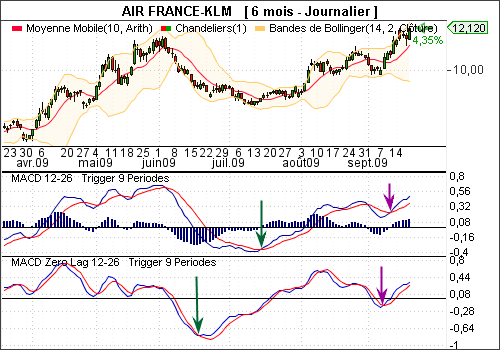

Example

Interpretation

The interpretation of MACD Zero Lag is identical to that of the classic MACD.