Technical Indicators

Commodity Selection Index

The Commodity Selection Index (or CSI) is a momentum indicator. It was developed by J. Welles Wilder and presented in his book New Concepts in Technical Trading Systems in 1978.

The name of the indicator reflects its initial purpose: to help select "Futures" commodity contracts for short-term trading.

The CSI is derived from the Directional Movement Index (DMI).

Calculation Method

CSI = ADXR * STR * K

where:

- ADXR: ADX of the "Directional Movement Index" for period p

- STR: Moving Average of the "True Range" over period p

- K: a constant representing the potential monetary variation of the future contract equal to

V / M * (1 / (150 + C)) * 100

with

V: the contract variation value expressed in monetary units for one cent of the monetary unit

M: the margin used in the contract in monetary units

C: the commission cost in monetary units

Note: Axial Finance sets the constant K = 100 by default

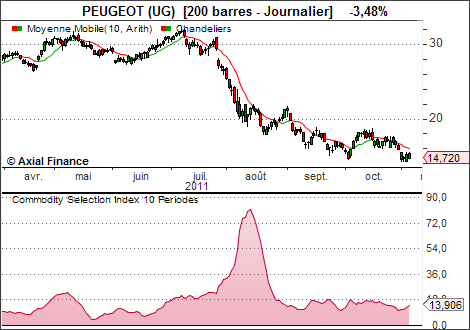

Example

Interpretation

A high CSI means that the commodity has a strong trend and high volatility.- The trend characteristic comes from the ADXR factor of the Directional Movement factor.

- The volatility characteristic comes from the STR factor.

Wilder's approach is to work with commodities that have a high CSI (relative to other commodities)

because these commodities are highly volatile. They therefore have the potential to "make the most money quickly".

But beware, this indicator is intended for those who can assume the risk associated with high

volatility.