Technical Indicators

Average True Range

The Average True Range (or ATR) is an indicator introduced by J. Welles Wilder in his book New Concepts in Technical Trading Systems. It is based on price volatility.

The Average True Range represents the Exponential Moving Average of "True Range" values for a given period.

The "True Range" is defined by Welles Wilder as the greatest of the following three differences:

- Today's high - Today's low

- Yesterday's close - Today's high

- Yesterday's close - Today's low

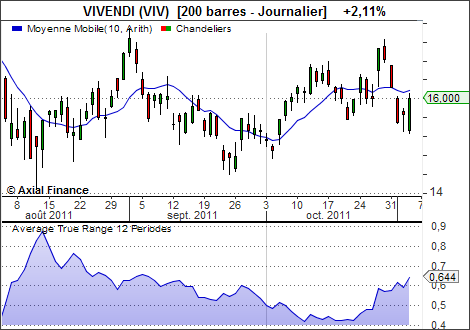

Example

Interpretation

Like most volatility indicators, a high ATR indicates strong market pressure on the security.A low ATR means, conversely, low volatility for the security.

The ATR can be interpreted using the same techniques used for volatility indicators.